Foodtech company Swiggy reiterated its plan to achieve contribution margin breakeven for Instamart between December 2025 and June 2026, even as its quick commerce segment faces intensifying competition and trails rival Blinkit in growth and scale.

“We believe this category will continue to see heightened competition. One major player entered last year, and another has just entered. But if you look at the history of this space, it hasn’t significantly impacted the growth of the top players,” said Sriharsha Majety, MD and CEO of Swiggy, in a post-earnings call.

Considering quick commerce a hyperlocal assortment play—which requires new players to offer the right selection in the right area through a supply chain built for speed—Swiggy expects competition to tighten in the future.

“Their ability to make an inroad in the market will be less. We still believe the top players in this particular area will only determine the investment in this market, as well as our ability to respond to that,” said Majety.

The Bengaluru-based foodtech major is banking on operational leverage from its existing infrastructure and a strategic pivot toward high-value orders as it charts a path to profitability for Instamart.

Rather than expanding aggressively, Swiggy is taking a measured approach to dark store expansion, having already built a network of 4.3 million sq. ft. across 127 cities. This footprint, it says, is sufficient to double the gross order value (GOV) without the need for further capacity addition.

A key lever in this strategy is the 26% annual rise in average order value (AOV), which the company attributes to habit-forming initiatives like Max Saver, a programme designed to encourage larger, bundled purchases.

According to Swiggy, this reflects a growing trend of consumers moving a larger share of their household wallet to quick commerce platforms—not just for groceries, but also for non-grocery, higher-margin categories.

In Q1 FY26, the non-grocery mix rose to 18.5% of Instamart’s GOV, up from 7% a year earlier. Swiggy expects this shift to unlock better monetisation opportunities through improved take rates, brand advertising, and seller partnerships over the coming quarters

.thumbnailWrapper{

width:6.62rem !important;

}

.alsoReadTitleImage{

min-width: 81px !important;

min-height: 81px !important;

}

.alsoReadMainTitleText{

font-size: 14px !important;

line-height: 20px !important;

}

.alsoReadHeadText{

font-size: 24px !important;

line-height: 20px !important;

}

}

Mulls inventory-led model

Just like its peer Blinkit, Swiggy might consider moving to an inventory-led model for its quick commerce business in future, said CFO Rahul Bothra.

He added, “We have more than doubled our domestic ownership to cross 40% in a very short time with increased participation of domestic fund houses. There could be an actual evolution that, at some point in time in the future, we may consider our ability to also open up to an inventory-led business model.”

Bothra expects benefits from this shift will see an improvement of roughly 50 to 70 basis points in the economics of quick commerce, adding that the upsides aren’t meaningfully high for Swiggy to consider inorganic moves.

According to FDI rules, ecommerce players with over 50% of domestic ownership are allowed to operate inventory models.

From equal to underdog

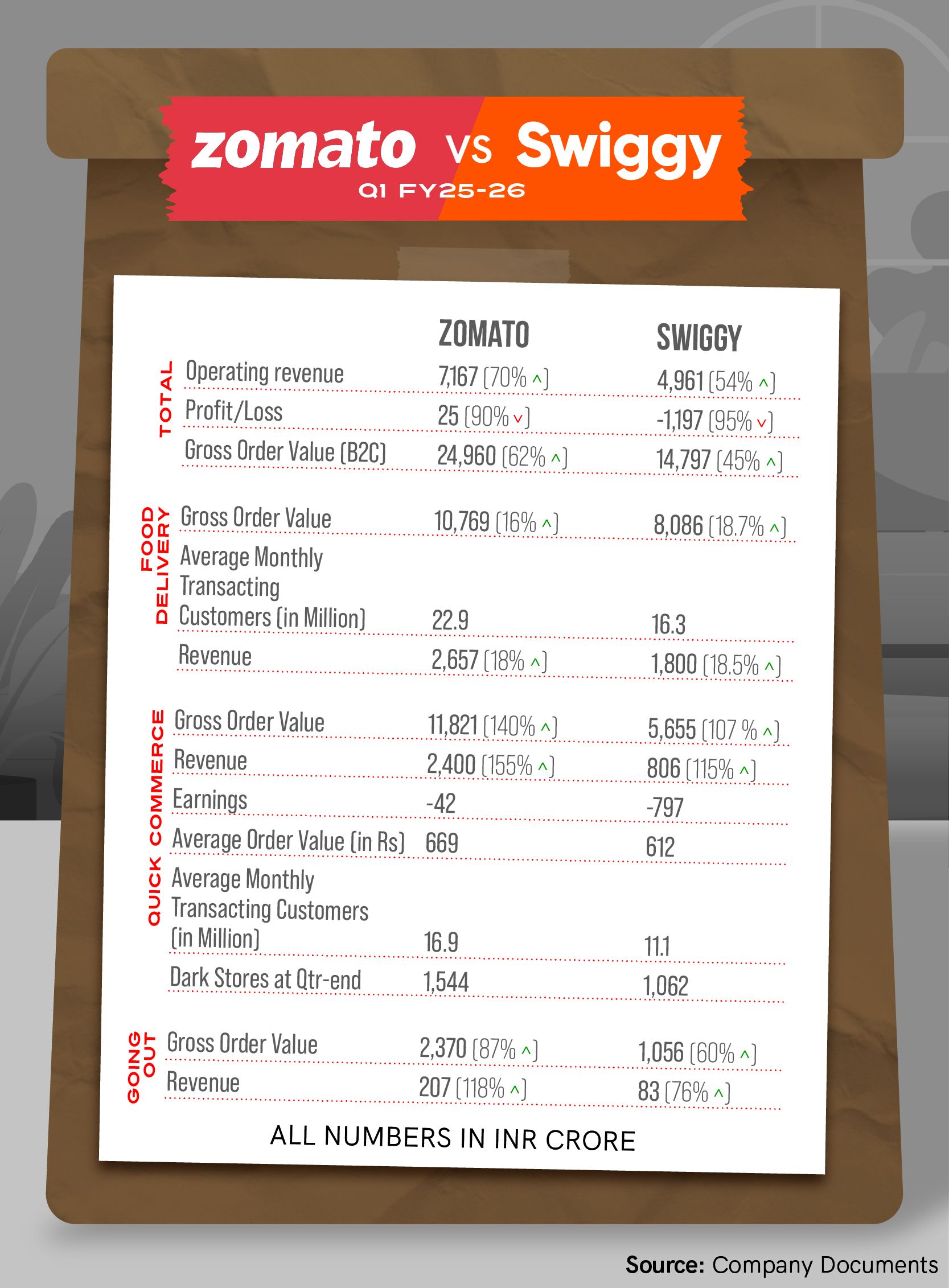

In Q1 FY26, both Zomato-parent Eternal and rival Swiggy posted strong topline growth, driven by continued momentum in the quick commerce segment.

However, Blinkit now appears to be pulling decisively ahead of Instamart on both revenue and user growth, even as the players continue to burn capital to capture market share.

Eternal reported Rs 7,167 crore in consolidated revenue from operations, up 70% YoY, while Swiggy posted a growth of 54% at a much smaller base to Rs 4,961 crore.

Blinkit reported a revenue of Rs 2,400 crore, more than double the Rs 942 crore it posted in the same quarter last year.

In comparison, Swiggy’s Instamart posted Rs 806 crore in revenue—just one-third the size of Blinkit’s contribution. On a sequential basis, Blinkit added nearly Rs 500 crore, while Instamart grew by only Rs 117 crore.

In terms of GOV, Blinkit surpassed Zomato’s food delivery GOV for the first time, underscoring its growing dominance.

Instamart, despite being an earlier entrant in the quick commerce race, is still trailing with a GOV of Rs 5,655 crore—behind Swiggy’s food delivery GOV of Rs 8,086 crore.

User traction also tilts in Blinkit’s favour. Monthly transacting users for Blinkit rose to 16.9 million, while Swiggy saw its MTUs double to 11.1 million.

While both players remain unprofitable in quick commerce, Blinkit reported a sequential improvement in losses, narrowing to Rs 42 crore from Rs 82 crore in Q4 FY25.

Instamart’s losses, by contrast, widened slightly to Rs 797 crore, nearly 20X that of Blinkit, as it realigns its strategy from infrastructure investment to infrastructure leverage.

Edited by Suman Singh