The journey of Chennai-based edtech firm Veranda Learning Solutions unfolds like a play in two acts.

The first act, Veranda 1.0—as Suresh Kalpathi, Executive Director and Chairman of the company, calls it—was about building the stage through acquisitions and expansion in both the offline and online spaces.

From its incorporation in 2018 to its public listing in 2022, the company moved quickly to acquire a slew of brands with strong regional presence or specialist expertise across four key verticals: K-12 academics, government test preparation, vocational training and upskilling, and commerce education.

These acquisitions—including JK Shah Classes, a leader in commerce and CA coaching; Edureka, a pioneer in live, instructor-led online training; and RACE, a dominant player in southern India for government exam coaching—were funded through a mix of debt and equity.

The group has integrated its offline classroom assets and digital-first platforms under a unified technology stack, centralising curriculum, analytics, and marketing, while preserving each brand’s identity. This strategy has helped Veranda scale enrolments across formats and geographies—there were 2 lakh learners as of FY25, mainly from Tamil Nadu, Kerala and Karnataka.

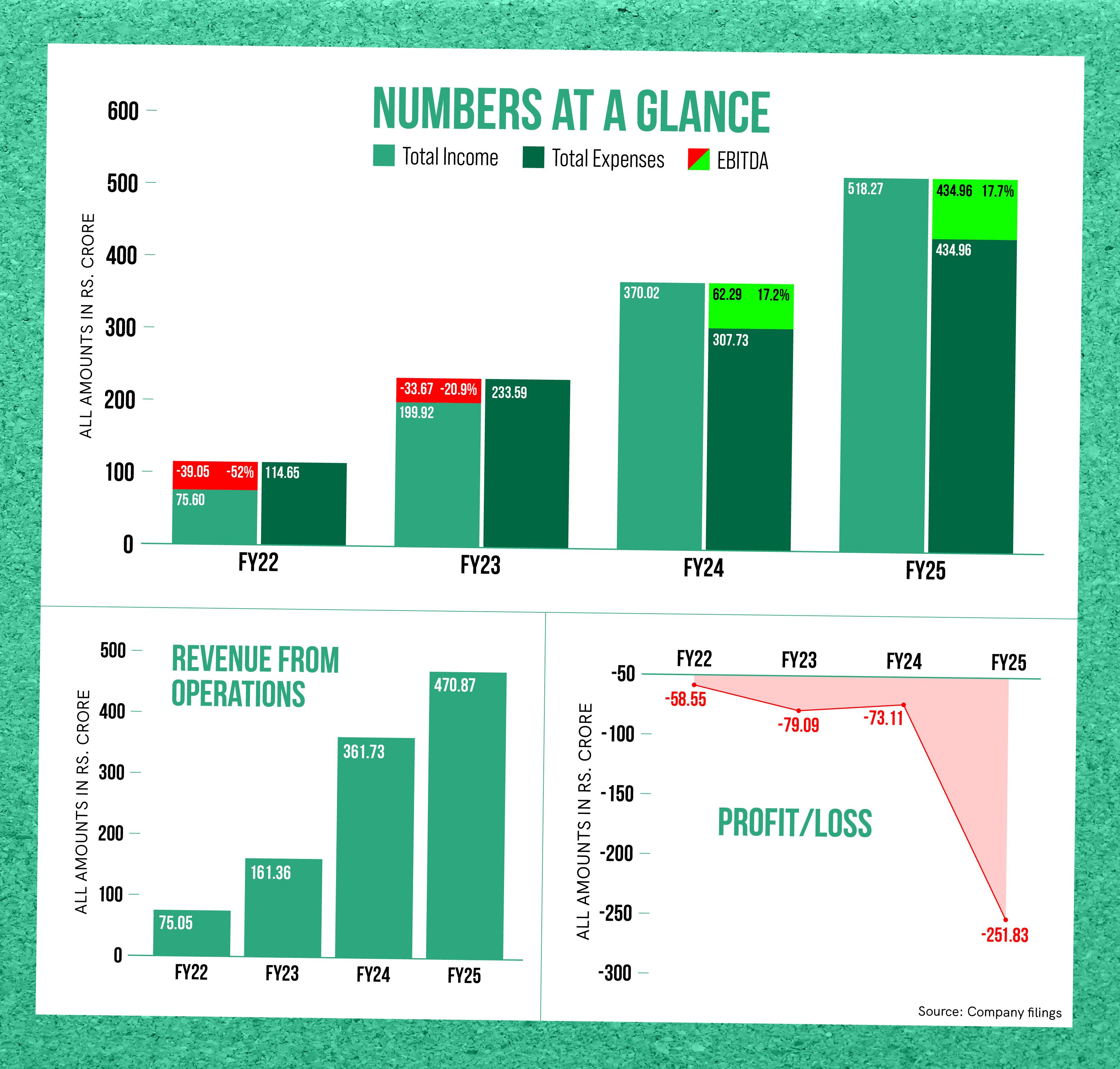

Veranda is now profitable at an operational level. FY25 marked the conclusion of the first act, with consolidated revenue reaching Rs 518.3 crore, up 40.1% year-on-year (YoY), and EBITDA rising to Rs 83.3 crore from Rs 62.3 crore in FY24.

A Rs 357-crore qualified institutional placement last month—87% of which was used to repay high-interest debt—helped the company’s commerce education vertical become debt-free, thus substantially deleveraging the group’s balance sheet.

Early signs from the first quarter of FY26 appear positive with group revenue growing 17% YoY to Rs 139 crore and EBITDA almost doubling to Rs 55 crore. Margins expanded to 40% through disciplined cost control and tighter cash-flow management, says Kalpathi.

Act 2 unfolds

The stage is now set for the second act—Veranda 2.0—to make assets perform better and deliver direct value to investors.

The plan is to unbundle the four verticals and list them as separate, independent companies on the stock exchanges, starting with Veranda’s best performing, debt-free asset—the commerce education vertical.

“We will, over a period of time, demonstrate significant value being created from each one of our four identified pillars,” says Kalpathi.

This shift from acquisition-led growth to disciplined value creation mirrors trends in other sectors, such as FMCG and technology, wherein conglomerates have spun off high-performing units to unlock valuation.

In India’s education space, where most large edtech firms continue to remain private, loss-making entities, a profitable, debt-free listing of a vertical would definitely stand out.

Kalpathi insists that the listing is not just “a great capital market move” but also one grounded in real business fundamentals and long-term demand for commerce education in India.

JK Shah and the big market opportunity

Veranda’s commerce education vertical provides comprehensive programmes for students pursuing careers in finance, accounting, and management, combining traditional and digital learning to cater to students across the country.

The vertical’s backbone is JK Shah Commerce Education Ltd, a 40-year-old name in commerce education with an alumni roster that boasts Union Minister Piyush Goyal and industrialist Kumar Mangalam Birla.

Veranda Learning acquired a 76% stake in JK Shah Classes for Rs 337.82 crore in October 2022, and it plans to acquire the remaining 24% by 2025.

Established in 1983, JK Shah Classes is a leading coaching institute for commerce students, specialising in chartered accountancy (CA), company secretary (CS), cost management accounting (CMA), and chartered financial analyst (CFA) courses. It operates both offline classroom centres across India and a comprehensive online platform, offering recorded lectures, live doubt-solving sessions, and personalised study plans.

Veranda is demerging JK Shah Commerce Education Limited into a separate, debt-free listed entity—offering direct exposure to investors and sharper strategic focus. The separation is expected to happen within the next seven to eight months.

For Kalpathi, the planned listing of JK Shah is the first proving ground for Veranda 2.0. “I wouldn’t be surprised if it trades at a valuation of a billion dollars,” he says, pointing to brand heritage and industry demand.

In Q1FY26, the commerce vertical delivered a revenue of Rs 71 crore, up 46% YoY, and EBITDA of Rs 47 crore, a 145% increase, with margins expanding sharply. An EBITDA of over Rs 200 crore is expected for FY27.

“In the space of commerce education we clearly have no competition at all,” Kalpathi says, arguing that the sector is fragmented and lacks a national player of scale capable of producing talent in the millions.

An edtech industry expert agrees that commerce coaching is a very big but largely underserved market. However, he adds that Kochi-headquartered Indian Institute of Commerce Lakshya is a strong player in the southern markets, Delhi and Uttar Pradesh.

Vocational and professional upskilling

Next comes vocational training and professional upskilling in finance and technology, which Veranda delivers via both online and offline models to cater to working professionals and college students.

A major transformation is underway in the upskilling segment, shaped by artificial intelligence, notes Kalpathi. “The type of skill set is dramatically changing,” he says, referring to generative AI tools reducing the demand for certain traditional programming skills.

In FY25, in response to market dynamics, Veranda’s upskilling vertical expanded its portfolio to offer postgraduate programmes (MBA, M.Sc) and other courses in DevOps and AI-focused skills, including genAI.

The company also offers diplomas, certifications and degree programmes in data science and technology, in partnership with Indian institutions such as IIM and IIT, and global universities Purdue, Illinois Institute of Technology, and University of Technology Sydney.

In Q1FY26, the vocational and professional segment delivered a revenue of Rs 35 crore, up 10% YoY, with EBITDA steady at Rs 6 crore.

Rather than pursuing acquisitions, the company is focused on scaling its existing portfolio, which includes brands such as Edureka, Six Phrase and PHIRE. “We don’t need more assets… We can build the vertical with what we got,” says Kalpathi.

The goal is to create a zero-debt, Rs 100-crore EBITDA business in about 18 to 24 months, with profits funding expansion without debt or dilution.

“The challenge is to keep pace with shifting industry demands… If it can meet its EBITDA target and keep its training relevant, this pillar could be the next to stand alone on the public markets,” says an industry observer.

K-12 school management expansion

In the K-12 segment, Veranda has taken on the role of an operator, managing existing schools that have been struggling to stay afloat. It is an asset-light model without the hassles of buying land or buildings and without taking on debt. The company currently manages six schools across Chennai, Coimbatore, Tiruchirappalli, and Bengaluru, under BVM Global Schools.

Many of these schools have been facing issues with enrollment and finances and competition from chains of schools with modern facilities and a diverse curriculum. Some of them are also run by ageing trustees without any succession plan.

Veranda brings to the table professional management, pedagogy and content, and extracurricular programmes, including sports, while keeping the school’s local identity intact.

The sports programme covers 14 disciplines with national-level coaches, while STEM integration, including robotics, runs from grade one to twelve. It also offers career-centric programmes in law, design and entrepreneurship to keep older students engaged and industry-equipped.

Kalpathi says the model benefits from centralised resources. Curriculum design, teacher training, technology platforms and extracurricular programmes are shared across the Veranda school network, reducing costs and improving quality. The curriculum is delivered via a blend of online tools (for enrichment and assessments) with in-class teaching tailored to the needs of every school’s needs.

“If we are able to get all this done, you have set up somebody for success,” says Kalpathi, underscoring the formative role schools play in shaping a child’s career trajectory.

FY25 saw strong momentum in the academics vertical, with a 239% YoY jump in revenue in Q4. In Q1FY26, revenue more than doubled to Rs 10 crore.

Going forward, growth is expected to be driven by 5,400+ students on the rolls, new leadership, and focus on integrated courses rollout, academic upgrades, and digital integration.

“We will expand aggressively by taking over operating management of schools… asset light, no leverage, no equity dilution,” says Kalpathi.

The focus right now is on southern India, where Veranda has strong market knowledge and relationships, before expanding to other regions.

Government test preparation

In the government exam preparation market, Veranda has a noticeable presence in southern India. Through its RACE and Talent brands, the company has trained a large number of candidates for roles in banking and other public sector jobs. Delivery is predominantly offline, matching the preferences of students in smaller towns for structured, in-person instruction, with peer support and immediate faculty access.

“If you look at banks, close to two out of three people who get a job from Tamil Nadu are my students,” Kalpathi says with pride.

Accessibility is the cornerstone. Course fee is kept affordable to attract students from Tier II and III towns, many of whom are the first people in their family to pursue such careers. In some places, about 80% of the cohort are women—a reflection of the fact that “families prefer government jobs for them” due to stability and social respect, Kalpathi points out.

Hiring slowdown in the private sector—compounded by concerns of AI’s impact on certain roles—has strengthened the appeal of secure, pensionable employment in the government. Government exam prep is counter-cyclical: demand often rises during periods of economic uncertainty.

While it is strong in southern India, scaling beyond this region could be challenging for Veranda, cautions an industry expert. Local players are well entrenched in most regions, making expansion into markets like Delhi and Kolkata costly and complex, he adds.

However, for now, Veranda’s priority is to consolidate its leadership in the south before expanding elsewhere.

In FY25’s final quarter, the segment’s EBITDA rose 139% YoY to Rs 8.6 crore despite a 20% revenue decline. In Q1FY26, government test-prep revenue fell 31% YoY to Rs 23 crore, with EBITDA moving from Rs 5 crore in Q1FY25 to break-even.

The rebound plan involves expanding to 12,000+ exam takers through regional focus and institutional tie-ups to deepen reach and enhance outcomes.

Looking ahead

Kalpathi’s vision for Veranda over the next five years is aimed at delivering value to investors, educators, and students alike. Early backers, he says, should see “anything between 10 to 20 times” their investment over the next five years.

The current quarter (Q2) is showing signs of sustained demand, and the company expects a consolidated revenue of Rs 650 crore in FY26 revenue.

Even as Veranda pursues its financial goals, all programmes, Kalpathi insists, will remain affordable and accessible, especially for students from less privileged backgrounds.

As he looks at the macro picture, Kalpathi has a candid take on the education sector at large, which has for long remained fragmented and dominated by regional players, and seen many boom-and-bust cycles. Profitability continues to elude many players in the edtech industry.

“After 30–35 years, the education sector has not created world-sized companies,” Kalpathi observes, adding that Veranda will be a strong contender to change the scenario, provided it can balance disciplined operations with sustained innovation.

“The goal is to create something of eminence within the four pillars we have chosen, where we get into the top five or even the top three in India,” he remarks.

A seasoned edtech expert opines, “Veranda’s stepwise approach of building profitable, debt-free verticals before pursuing expansion offers a measured and sustainable growth path. Its diversified segments provide a natural hedge, balancing steady cash flows, strong growth opportunities, and recurring revenues across verticals.”

(Cover image and infographics designed by Nihar Apte)

Edited by Swetha Kannan